How Can Young Indians Save Money When Prices Keep Rising?

Editorial Team7 min read

Loading…

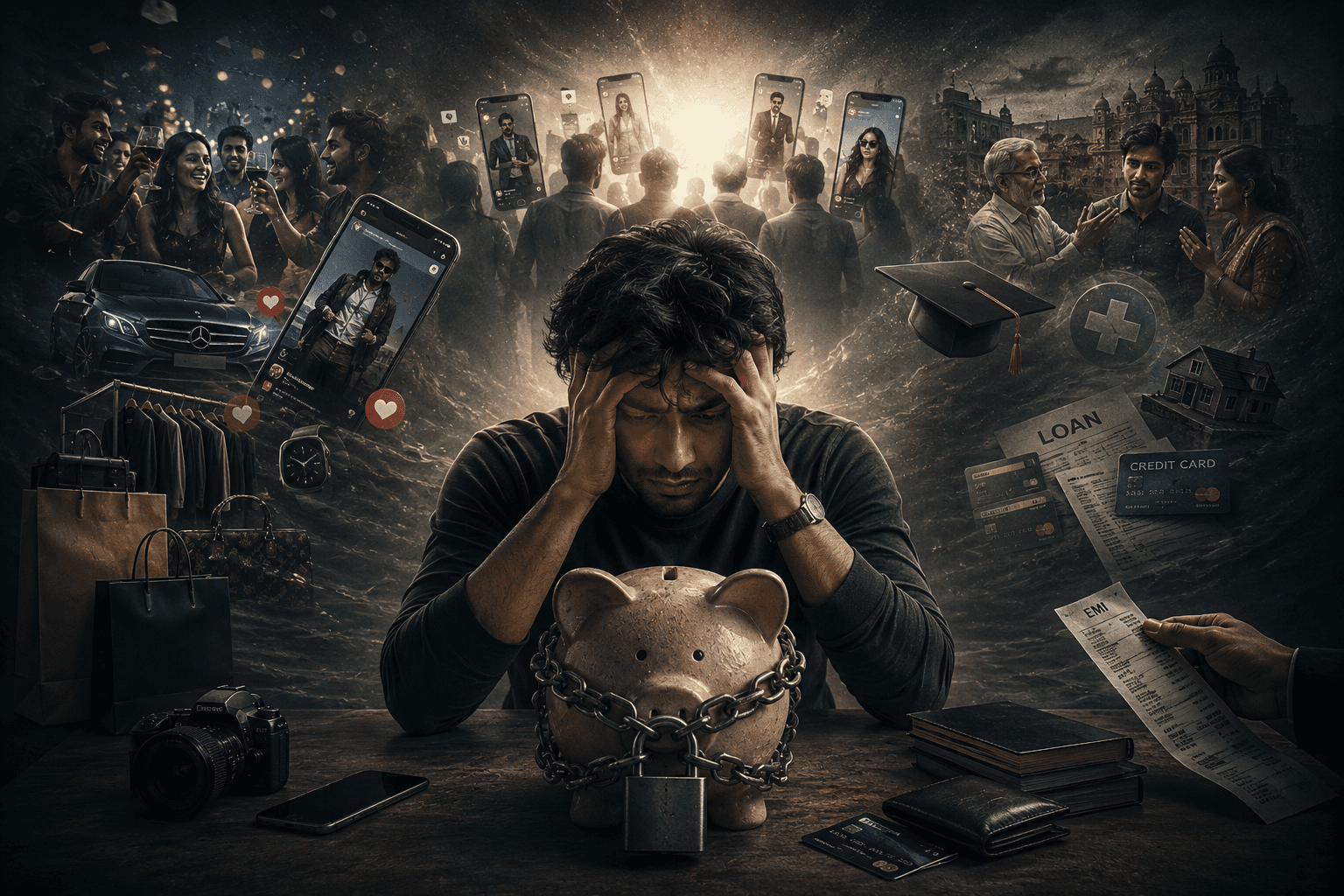

The first salary hits the account. A rush of freedom. The fancy dinner at a mall in Saket. The new sneakers from that Instagram ad. The feeling that you’ve finally made it. Then comes the second week. The auto-rickshaw fare has gone up again. The coffee that used to be a treat is now a luxury. You check your banking app. The balance is a frighteningly small number. You start calculating. If I skip the weekend movie, I can afford rent. If I stop ordering in, I might have enough for the commute. The numbers just don't fit. The prices keep climbing, but the paycheck stays the same. You stare at the screen, feeling a knot in your stomach. Why does it feel like I'm running a race where the finish line keeps moving further away?

When prices go up, it isn't just a math problem; it is a mental battle. Most of us experience something called "lifestyle creep." This happens when our income increases, and we unconsciously raise our spending to match it. But when inflation hits, we face the opposite problem. We are trying to maintain a lifestyle that our current budget can no longer support.

Psychologists suggest that we often tie our identity to what we consume. For a young professional in India, buying a specific brand of phone or eating at a trendy cafe isn't just about the product—it is about feeling like they belong to a certain social class. When prices rise, giving up these things feels like losing a part of who we are. This creates a state of mental friction. We know we should save, but the fear of "missing out" or appearing "broke" to our peers keeps us spending. We aren't just buying a latte; we are buying the feeling of being "successful."

There is also the concept of "decision fatigue." Every time you go to the grocery store and see that the price of oil or pulses has jumped by ten rupees, your brain has to make a new choice. Should I buy a cheaper brand? Should I buy less? Should I switch to a different grain? Doing this a hundred times a day drains your willpower. By the time you reach the end of the day, your brain is tired, making you more likely to make an impulsive purchase—like a late-night Zomato order—just to feel a momentary sense of reward. This is why we often spend the most money when we are the most exhausted.

Furthermore, we often fall into the trap of "present bias." This is the tendency to value immediate rewards over future gains. A cold coffee today feels more valuable than a retirement fund thirty years from now. When inflation makes the future feel uncertain, the brain instinctively wants to enjoy everything now because tomorrow feels too expensive to plan for. This creates a cycle of "revenge spending," where we spend money we don't have to compensate for the stress of a demanding job or a bleak economic outlook.

Beyond the psychology of spending, there is the "anchoring effect." Our brains anchor to the price we used to pay. When a meal that was 200 rupees becomes 300, we don't see it as a 300-rupee meal; we see it as a 100-rupee loss. This creates a constant sense of deprivation, even if we are still technically spending more than we did a year ago. This mental friction makes us feel poorer than we are, leading to a state of chronic financial stress that affects our sleep, our productivity, and our relationships.

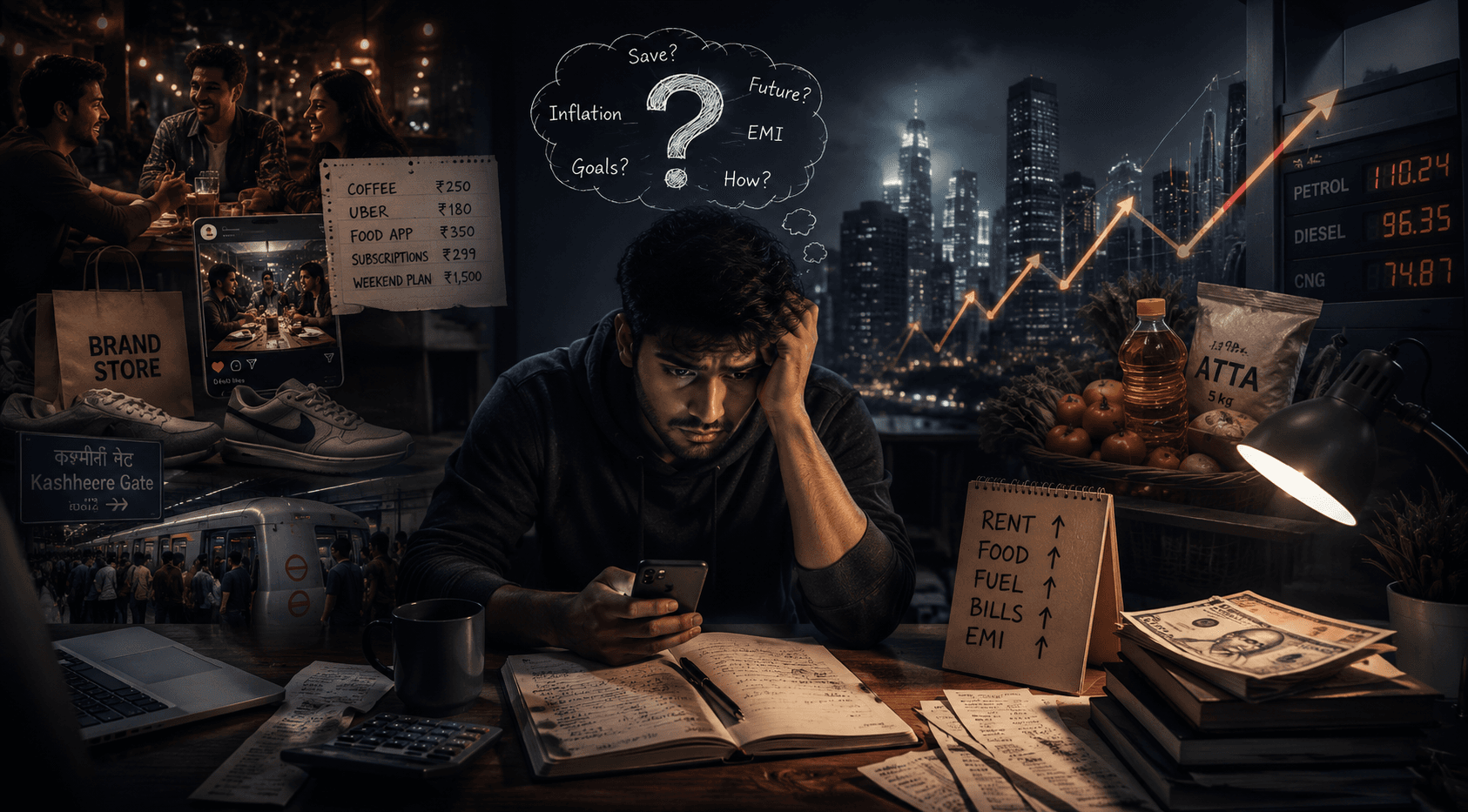

Imagine Ishaan, a 23-year-old software engineer living in a shared PG in Bengaluru. He moved there with big dreams and a decent starting package. For the first six months, he felt wealthy. He spent his weekends exploring breweries and took Ubers to avoid the chaos of the buses. But slowly, the "hidden" costs started piling up. The rent for his PG increased without warning. The cost of a basic meal at the local mess went up. Suddenly, his "fun money" was being eaten by survival costs.

Ishaan doesn't tell his parents because he doesn't want them to worry, and he doesn't tell his friends because they all seem to be spending effortlessly. He spends his Sunday nights staring at an Excel sheet, feeling a deep sense of failure. He wonders if he is bad with money or if the world is simply becoming too expensive to live in. The emotional toll is a constant, low-level hum of anxiety that follows him into every meeting. He finds himself calculating the cost of a tea break in his head, wondering if he can afford the extra biscuit today. The gap between the life he presents on Instagram and the life he lives in his PG becomes a source of profound loneliness.

Then there is Ananya, a postgraduate student in Delhi who relies on a monthly allowance and a small freelance gig. She is careful, but the inflation surge has hit her hard. The price of the metro, the cost of photocopies for her notes, and the rising price of basic vegetables have turned her budget into a puzzle with missing pieces. She finds herself skipping meals or avoiding social gatherings because she cannot afford the "minimum spend" at a cafe.

When her friends suggest a trip to Kasol, she makes up an excuse about being busy with assignments. The hurt isn't just about the money; it is the feeling of isolation. She feels like she is falling behind in a life race she didn't even sign up for. The self-doubt creeps in—she starts questioning if her degree will even lead to a salary that can keep up with the cost of living. She feels a sense of shame when she has to ask for a small extension on her rent or when she sees her peers buying the latest gadgets. This isn't just about budgeting; it is about the fear that the middle-class dream is slipping away, replaced by a cycle of endless hustle and zero growth.

Consider also the pressure of "social performance" in cities like Mumbai or Gurgaon. Imagine a young professional who feels the need to dress a certain way to fit into the corporate culture. The cost of dry cleaning, the pressure to own specific brands, and the expectation to contribute to group dinners at expensive restaurants create a financial treadmill. Every time they try to save, a wedding or a birthday party comes up, and the fear of being judged for saying "I can't afford it" pushes them to swipe a credit card. The resulting debt isn't just a financial burden; it's a mental weight that makes every notification from a banking app feel like a jump-scare.

What to do right now Open your banking app and look at your last thirty days of transactions. Highlight every expense that didn't actually make your life better or healthier. Once you see the total, don't judge yourself—just decide on one specific "leak" you will plug starting tomorrow morning.

How Can Young Indians Save Money When Prices Keep Rising? Can Young Indians Save Money When Prices Keep Rising can improve when you apply one clear step consistently and track progress for at least two weeks.

The first salary hits the account. A rush of freedom. The fancy dinner at a mall in Saket.

The first salary hits the account. A rush of freedom. The fancy dinner at a mall in Saket.

When prices go up, it isn't just a math problem; it is a mental battle. Most of us experience something called "lifestyle creep.

Imagine Ishaan, a 23 year old software engineer living in a shared PG in Bengaluru.

The 50/30/20 Rule: Allocate 50% of your income to needs (rent, bills), 30% to wants, and 20% to savings or debt.

The 50/30/20 Rule: Allocate 50% of your income to needs (rent, bills), 30% to wants, and 20% to savings or debt.

Reader membership

Want bonus guides and early access? Purchase a Thinkora Reader Pass.

Keep reading

Bookmark this site, explore more in the same lane, or tell a friend who overthinks at 2 AM — that is how good ideas spread without ads.