Why Do People Struggle to Save Money?

Editorial Team7 min read

Loading…

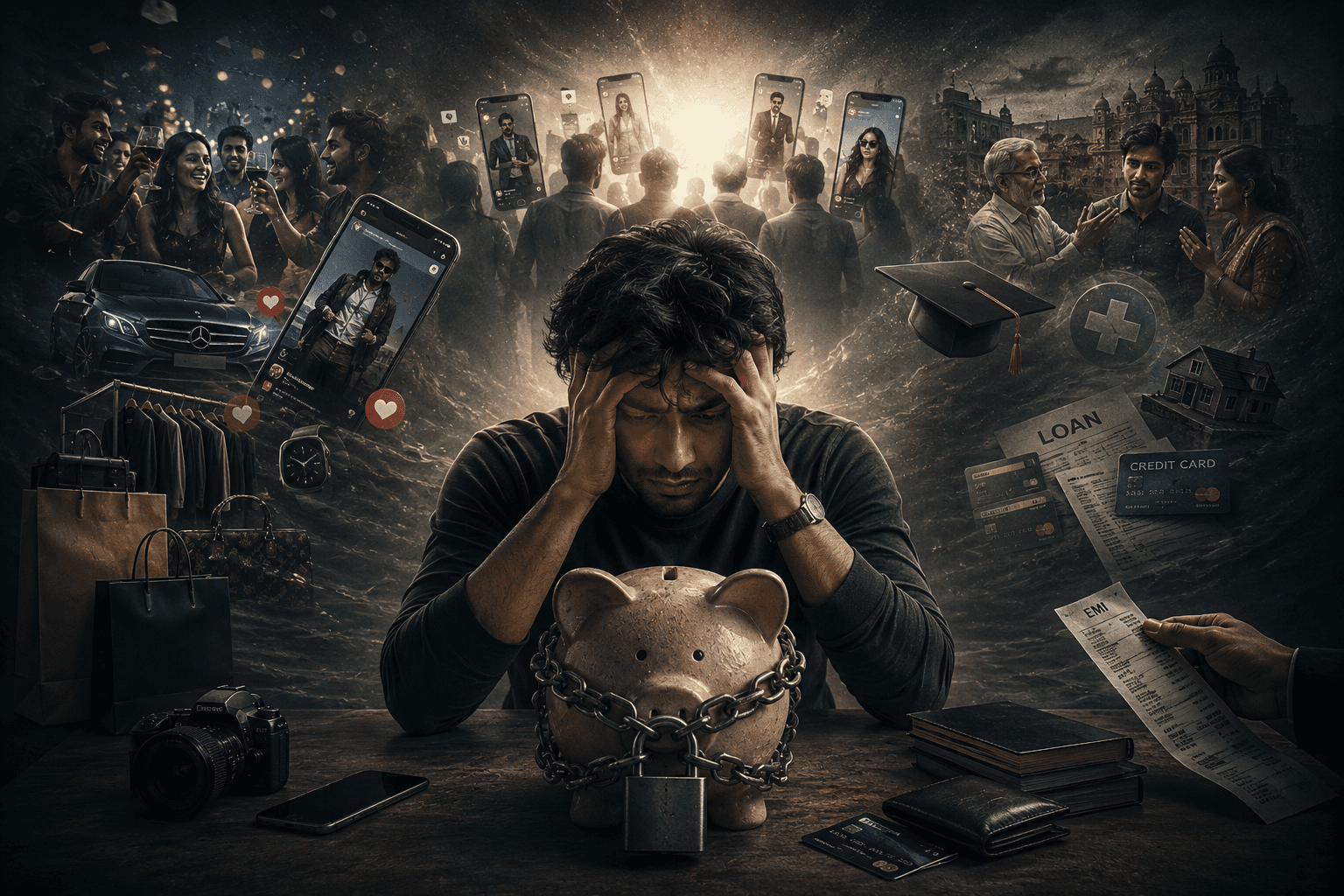

It starts with a first salary. A sense of freedom. The ability to spend on anything. Then reality hits. Bills to pay. Rent to cover. EMI payments due. No money left to save. The guilt sets in. Why can't I save? What's wrong with me? Is it even possible to save? The pressure to save can be overwhelming, and the feeling of failure can be debilitating. It's a constant battle between wanting to enjoy the present and securing the future. The question remains, what's holding us back from saving?

Psychologists believe people struggle to save due to many reasons. Some lack a clear financial goal. Others are held back by impulse purchases. Some fear missing out on experiences. Others feel overwhelmed by debt. The key to saving is creating a mindset shift. It's about understanding that saving is not just about money, but about freedom and security. When we prioritize saving, we're investing in our future selves. We're giving ourselves the gift of peace of mind. Saving is a habit that can be developed over time with practice and patience. It's essential to start small and be consistent. Setting aside a fixed amount each month, like a SIP, can make a significant difference in the long run. The power of compounding can work in our favor, helping our savings grow exponentially. However, it's crucial to avoid common pitfalls like dipping into savings for non-essential purchases. By being mindful of our spending habits and making conscious financial decisions, we can overcome the obstacles that prevent us from saving. It's also important to recognize that saving is not a one-size-fits-all approach. What works for someone else may not work for us. We need to find a saving strategy that suits our lifestyle and financial goals. Whether it's using the 50/30/20 rule or implementing a zero-based budget, the key is to find a system that works for us and stick to it. By doing so, we can develop a healthy relationship with money and make progress towards our financial goals. Additionally, understanding the concept of delayed gratification is essential. It's about prioritizing long-term benefits over short-term pleasures. When we delay gratification, we're essentially investing in our future. We're giving up something we want now for something we want more later. This mindset is crucial for saving, as it helps us make sacrifices in the present for a more secure future. Moreover, the role of emotions in saving cannot be overlooked. Emotions like fear, anxiety, and guilt can be significant barriers to saving. When we're overwhelmed by these emotions, we may feel paralyzed, and our ability to make rational financial decisions is impaired. It's essential to acknowledge and address these emotions, rather than letting them control our financial decisions. By recognizing the emotional aspects of saving, we can develop a more compassionate and realistic approach to our financial goals.

Picture this: you're a young professional in Mumbai, earning a decent salary, but struggling to make ends meet. Your rent is high, and you have to pay EMI for your education loan. You want to save, but it seems impossible. You feel guilty for not being able to save, and you start to doubt your financial decisions. Imagine you're in Delhi, and you've just started your first job. You're excited to earn your own money, but you're not sure how to manage it. You're tempted to spend on luxuries, but you know you should save. You feel confused and unsure about how to prioritize your expenses. In both scenarios, the emotional impact is significant. The stress and anxiety of not being able to save can be overwhelming. It's essential to acknowledge these feelings and address them. By recognizing that saving is a challenge, we can start to work on solutions. We can start by tracking our expenses, creating a budget, and setting realistic financial goals. We can also seek support from friends, family, or a financial advisor. In India, saving is not just about individual efforts; it's also about cultural and social factors. We often prioritize spending on family and social obligations over saving. However, it's crucial to find a balance between our responsibilities and our financial goals. By being mindful of our spending habits and making conscious financial decisions, we can overcome the obstacles that prevent us from saving. For instance, we can use the festival of Diwali as an opportunity to review our finances and set new savings goals. We can also use the Indian government's initiatives, such as the Pradhan Mantri Jan Dhan Yojana, to our advantage and take advantage of the benefits offered. By taking small steps towards saving, we can make a significant difference in our financial lives. Furthermore, the role of technology in saving cannot be overlooked. With the rise of digital payment systems and mobile wallets, it's easier than ever to track our expenses and make smart financial decisions. We can use apps like Mint or Spendee to monitor our spending habits and identify areas where we can cut back. We can also use automated savings tools like SIPs or systematic transfer plans to make saving easier and less prone to being neglected. Additionally, the concept of community saving can be a powerful tool in India. We can join savings groups or start our own with friends and family. This can provide a sense of accountability and motivation, as well as a support system to help us stay on track with our financial goals. By leveraging these tools and strategies, we can make saving more accessible and achievable, even in the face of cultural and social pressures.

What to do right now Take a deep breath and acknowledge your struggles with saving. Recognize that it's okay to start small and that every step counts. Begin by tracking your expenses and creating a budget. Set a realistic financial goal, like saving a certain amount each month. Remember, saving is a journey, and it's essential to be patient and kind to yourself. By taking small steps towards saving, you can develop a healthy relationship with money and make progress towards your financial goals. Start today, and watch your savings grow over time. Don't be too hard on yourself if you slip up – simply acknowledge the setback and get back on track. Celebrate your small wins, and use them as motivation to keep moving forward. With time and practice, saving will become a habit, and you'll be on your way to achieving financial freedom.

Why Do People Struggle to Save Money? Do People Struggle to Save Money can improve when you apply one clear step consistently and track progress for at least two weeks.

It starts with a first salary. A sense of freedom. The ability to spend on anything.

It starts with a first salary. A sense of freedom. The ability to spend on anything.

Psychologists believe people struggle to save due to many reasons. Some lack a clear financial goal.

Picture this: you're a young professional in Mumbai, earning a decent salary, but struggling to make ends meet.

Start small: set aside a fixed amount each month Be consistent: make saving a habit Avoid impulse purchases: think before you buy Use the 50/30/20 rule: allocate your income wisely Review and adjust: regularly check your budget and make changes as needed Take advantage of tax benefits: utilize tax saving options like PPF and NPS Automate your savings: use t…

Start small: set aside a fixed amount each month Be consistent: make saving a habit Avoid impulse purchases: think before you buy Use the 50/30/20 rule: allocate your income wisely Review and adjust: regularly check your budget and make changes as needed Take advantage of tax be…

Optional support

Found this helpful? Help us keep Thinkora free for everyone.

Keep reading

Bookmark this site, explore more in the same lane, or tell a friend who overthinks at 2 AM — that is how good ideas spread without ads.