Why "Buy Now, Pay Later" Is Quietly Becoming a Debt Trap for Millions

Editorial Team9 min read

Loading…

You're at checkout. The total feels a little steep, but then you see it: four small payments instead of one big one, no interest, approved in seconds. You tap it without a second thought. That's the entire design of buy now, pay later (BNPL) — and it's exactly why so many people are waking up to balances they didn't quite see coming.

BNPL isn't a niche payment option anymore. Roughly half of U.S. adults have used a BNPL service, and providers like Klarna, Afterpay, Affirm, and PayPal Pay Later now show up at checkout for everything from concert tickets to groceries. The convenience is real. So is the risk. Late payments among BNPL users have climbed for two years running, and the federal rules meant to protect consumers have largely been rolled back — which means the burden of using these loans wisely falls almost entirely on you.

This isn't a warning to never use BNPL. It's a clear-eyed look at how the product actually works, what the research says about who gets hurt by it, and how to use it — or avoid it — without it quietly reshaping your budget.

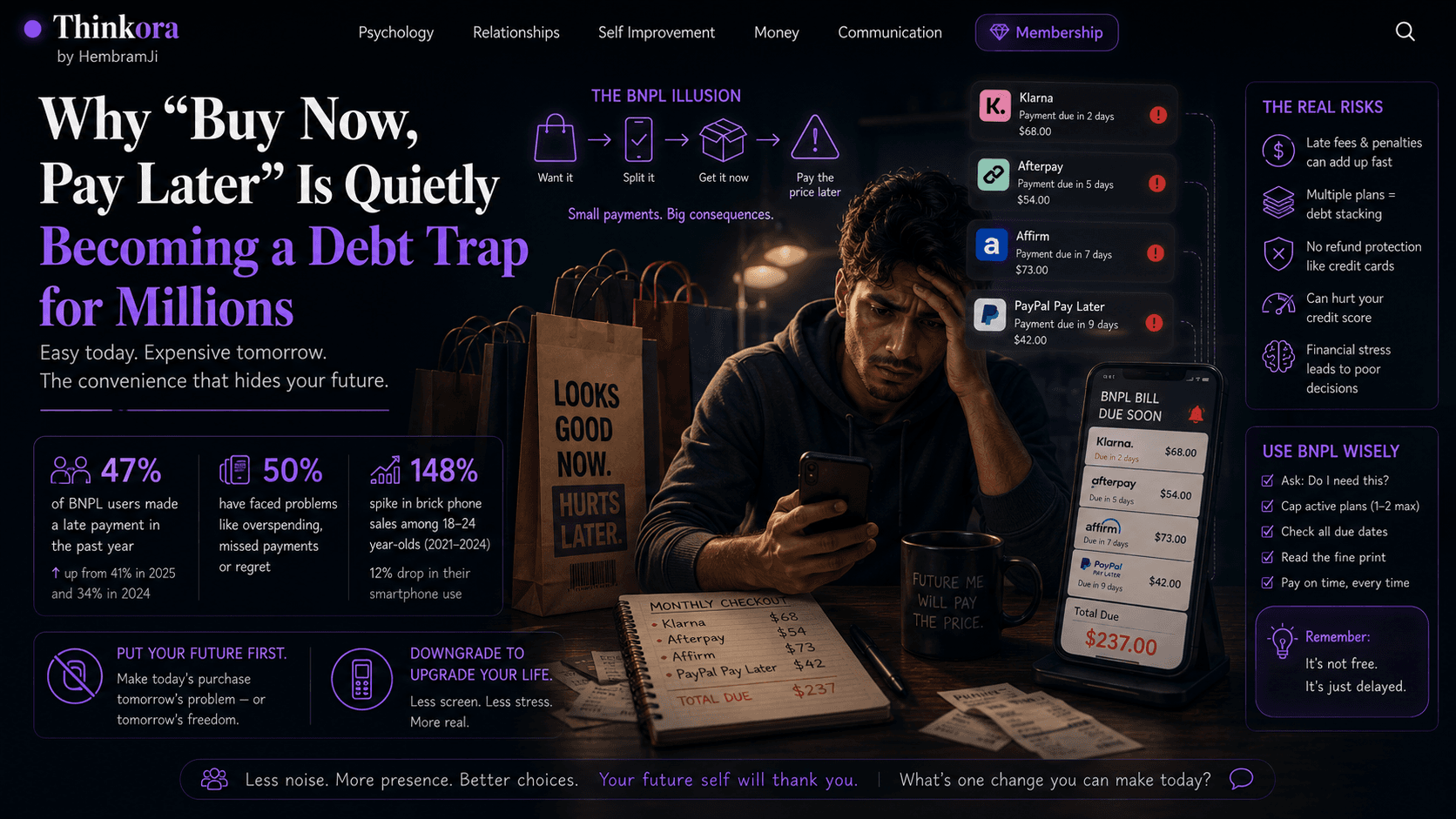

BNPL is a short-term installment loan, most commonly structured as "pay in 4": a purchase is split into four equal payments, usually due every two weeks, with no stated interest if you pay on time. It was popularized by the Swedish fintech Klarna and has since spread through competitors including Afterpay, Affirm, Sezzle, and PayPal Pay Later, along with countless retailer-specific plans.

The pitch is simple — spread out the cost, skip the interest, get the item today. What makes it different from a credit card is also what makes it easy to lose track of: each BNPL plan lives in its own app, with its own due date, its own lender, and — until recently — almost none of the dispute or refund protections that come standard with a credit card.

According to LendingTree's 2026 Buy Now, Pay Later Report, 47% of BNPL users say they've made a late payment in the past year — up from 41% in 2025 and 34% two years earlier. That's not a small drift; it's a trend line pointed the wrong way, two years in a row.

A separate Bankrate survey found that roughly half of BNPL users have run into some kind of problem — overspending, a missed payment, or regret over a purchase. And the habit isn't limited to splurge items anymore: multiple industry surveys now find a meaningful share of users leaning on BNPL for everyday essentials like groceries, not just discretionary purchases.

Part of the problem is structural, not just personal. Researchers who study the space use the term "debt stacking" — holding several BNPL plans across different providers at once. Because each plan is siloed in its own app, there's rarely a single place to see your total exposure the way a credit card statement shows one consolidated balance. A person managing three or four open plans is really managing three or four separate payment streams, each with its own due date. Surveys differ on exactly how common this is, but multiple studies agree it's now common enough to be a defining feature of how people actually use BNPL — not an edge case.

For a brief period, this mattered less, because BNPL was on track to get credit-card-style protections. In May 2024, the Consumer Financial Protection Bureau issued an interpretive rule stating that BNPL lenders were, in effect, credit card providers under the Truth in Lending Act — meaning they'd have to investigate disputes and issue refunds for returned merchandise, the same as a Visa or Mastercard issuer would.

That rule didn't survive. It was challenged in court by the BNPL industry's trade association, and in May 2025 the CFPB withdrew it. The agency has since said it does not intend to reissue a revised version. Two internal CFPB studies have even reached different conclusions about whether BNPL harms consumers, which tells you the research itself is still unsettled.

Some states aren't waiting on Washington. New York's BNPL Act, signed in 2025, introduces licensing requirements, fee limits, and data-privacy protections for providers operating in the state, and its Department of Financial Services published proposed implementing rules in 2026. Whether more states follow that model remains to be seen — but for now, protections largely depend on where you live, not on any single federal standard.

BNPL's appeal tends to spike exactly when people can least afford a misstep. A Bankrate survey found pessimism about personal finances at its highest level since 2018, driven largely by persistent price increases — and paying down debt was the most commonly cited financial goal in that same survey.

Research covered by the American Psychological Association points to a related pattern: people under financial strain often have less margin for error in spending decisions, and unsecured debt — the kind BNPL creates — is associated with worse financial wellbeing. That doesn't mean BNPL causes stress on its own. It means the product tends to be most attractive to people who have the least room to absorb a missed payment, which is a hard combination.

The experts who work directly with BNPL borrowers tend to converge on a few consistent habits:

None of this means BNPL is inherently bad. Used occasionally, for a planned purchase, with a clear repayment plan, it can be a genuinely interest-free way to manage cash flow. The risk shows up specifically when it becomes a default habit rather than a deliberate choice.

BNPL didn't get more dangerous overnight — it got more normalized, at the exact moment the regulatory guardrails around it got weaker. That combination is worth taking seriously, not by avoiding the product entirely, but by treating every "pay in 4" click with the same scrutiny you'd give an actual loan application, because that's what it is.

If you use BNPL regularly, try this today: open every BNPL app on your phone and write down each balance and due date in one place — a notes app, a spreadsheet, anything. If that list surprises you, that's useful information, not a judgment. It's also the first real step toward getting your BNPL use back under your control instead of the other way around.

[INTERNAL LINK: how to build an emergency fund on a tight budget] — if BNPL has been filling the gap for unexpected expenses, a small emergency fund tends to be a more durable fix.

What's your experience with buy now, pay later — helpful tool or slippery slope? We'd love to hear how you manage it in the comments below.

What to do right now What's your experience with buy now, pay later — helpful tool or slippery slope? We'd love to hear how you manage it in the comments below.

Why "Buy Now, Pay Later" Is Quietly Becoming a Debt Trap for Millions "Buy Now, Pay Later" Is Quietly Becoming a Debt Trap for Millions can improve when you apply one clear step consistently and track progress for at least two weeks.

You're at checkout. The total feels a little steep, but then you see it: four small payments instead of one big one, no interest, approved in seconds.

You're at checkout. The total feels a little steep, but then you see it: four small payments instead of one big one, no interest, approved in seconds.

According to LendingTree's 2026 Buy Now, Pay Later Report, 47% of BNPL users say they've made a late payment in the past year — up from 41% in 2025 and 34% two years earlier.

For a brief period, this mattered less, because BNPL was on track to get credit card style protections.

BNPL's appeal tends to spike exactly when people can least afford a misstep. A Bankrate survey found pessimism about personal finances at its highest level since 2018, driven largely by persistent price increases — and paying down debt was the most commonly cited financial goal in that same survey.

Ask two questions before you tap "pay in 4. "Buy Now, Pay Later" Is Quietly Becoming a Debt Trap for Millions can improve when you apply one clear step consistently and track progress for at least two weeks.

Found this helpful? Tap like — it helps us know what readers enjoy.

Share your thoughts. Comments appear after a quick review.

Loading comments…

Reader membership

Want bonus guides and early access? Purchase a Thinkora Reader Pass.

Keep reading

Bookmark this site, explore more in the same lane, or tell a friend who overthinks at 2 AM — that is how good ideas spread without ads.